Stocks have plummeted across the board. We are going to go into a recession. Everyone is going to die. Or not.

The simple fact is this too shall pass. For now, good firms with solid incoming cash flows, and bad firms with unserviceable debt and troubled cash flows are being treated roughly equally. Knowing the difference never had more value. About the only type of firms everyone agrees have become more valuable are those that directly benefit from the COVID-19: drug firms (Arcturus (NASDAQ:ARCT)), disposable mask and gown suppliers (Alpha Pro Tech (NYSEMKT:APT)), work and play from home internet facilitators (Netflix (NASDAQ:NFLX)), etc.

Cash And Margin

For those with cash sitting on the sidelines waiting to be deployed. Congratulations, you are the real winners here! But only if you actually deploy it. The personality that keeps cash on hand, tends to also be the personality that is too afraid to deploy it when times get tough. Don’t be that person. If you already had written trading and allocation rules which considered the situation of a greater than 20% loss in the market, dust it off and do that. For others, it’s time to consider suck it up, hold your nose, and be greedy when others are fearful. Just make sure you do it with logic and knowledge.

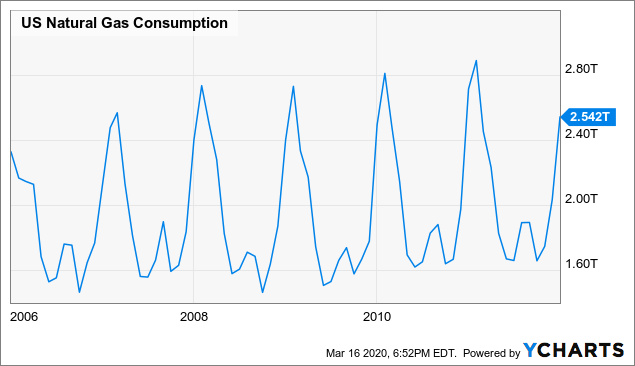

For instance, did you know while oil firms are in trouble, most whose main business is facilitating the transport of natural gas probably are not? Do you know why? Hint, look at this graph:

Without looking at the dates, can you tell where the Great Recession or 2015 oil price collapse are? For people with cash on the sidelines, now is the time to buy excellent companies at fair prices, but you need to know which companies those are.

Without looking at the dates, can you tell where the Great Recession or 2015 oil price collapse are? For people with cash on the sidelines, now is the time to buy excellent companies at fair prices, but you need to know which companies those are.

That however doesn’t apply in the same way for those considering extending margin. One needs to be very cautious with margin because by definition what is going on is irrational. Irrational can become even more irrational. More irrational can become crazy irrational. That guy on TV doesn’t know when it ends, I don’t know when it ends, and neither do you. Don’t pretend “it can’t get much worse.” It can. Or not.

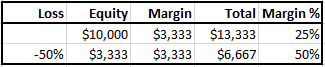

That being said, there is opportunity apparent. So, I’m not going to make a blanket statement that margin shouldn’t be used at all. In fact, going conservatively into margin near the end of a crash is one way to significantly increase your portfolio’s long-term return. However, when do you know it’s the end? Again, irrational can become crazy irrational, and you are not going to know when this crash has fully played out. Nobody, Fed included, raises the green flag. Thus, the amount of margin one adopts should be kept low enough that prices could fall another 50% without you getting margin calls. That equates to having no more than 25% on margin today.

Source: Author Calculations

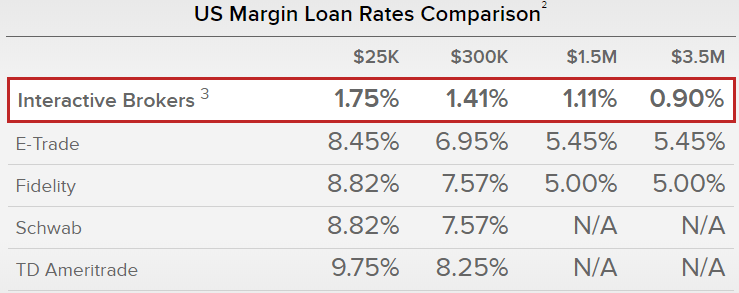

It also implies being willing to accept the 67% loss the above chart implies should it come to be. Nobody said getting rich is easy. The good news is if you are with Interactive Brokers, your margin is going to be very cheap.

You can actually do very, very well borrowing money at >2% to buy something that yields much more but is still reasonably safe. However, even here you need to be careful as Interactive Brokers can end up changing 50% max margin on a holding to 35%, 25% or even less without notice. It has been doing so with TNP, GLOP, and other preferred recently.

This may be one reason we are seeing some preferred and baby bonds become irrationally cheap. Because they aren’t allowed as much margin, they are getting liquidated as the most efficient means of meeting margin calls.

Thus, moving back to our all-cash buyers, these can be an excellent opportunity. If you have available cash, lower risk preferred and baby bonds should probably be the first place you look. Examples include: TGP.PB (yields 17.5%), TNP.PC (has a 34% YTM to its FTR clause), GLOP.PC (35% yield), GLOG.PA (16% yield), NSS (20% yield), GSLD (25% YTM), INSW.PA (13% YTM), ETP.PE (21% yield), NGLS.PA (28%), NS.PC (33%). These securities continue to get sold off, not so much because of fundamental weakness in the underlying firms, but instead due to fear and the technical reasons outlined above. Just be aware cheap can get cheaper. Don’t extend yourself so much that you can be blown out of a very good investment by a margin call at the worst possible point in time.

Also I need to disclose some of these securities go fixed to floating within a few years. I like fixed to floating because in a situation where we are still at 0% rates 2 years from now, I’m going to be fine “just” getting paid 6% as opposed to the 8% I started at.